Reading Time: minutes

The Philippines Is Ready for Its Industrial Moment

Why semiconductor, data centre, and advanced manufacturing companies, and the developers who want to serve them, should be looking at the Philippines as the next serious industrial destination in ASEAN.

The conversation around Southeast Asia’s industrial real estate market has been dominated by the same two names for the better part of a decade: Thailand and Vietnam. Both have earned their reputations. But as supply tightens in the Eastern Economic Corridor and Vietnam’s prime industrial zones fill up with China+1 relocations, a third market is quietly assembling the conditions for a step-change in industrial investment, and most occupiers haven’t fully priced it in.

Two separate but converging pressures are now driving that reassessment. The first is China+1: the well-documented push by global manufacturers to diversify production away from single-country concentration. The second is newer, more urgent, and carries higher stakes, Taiwan+1: the scramble by the global semiconductor industry to reduce catastrophic dependence on a single island that sits at the centre of the world’s most consequential geopolitical fault line.

The Philippines is positioned to benefit from both. But the Taiwan+1 case, in particular, deserves serious attention from any company whose product roadmap depends on semiconductor supply chain continuity.

The Philippines is no longer just a BPO economy. It is becoming a serious industrial destination, and the window to secure prime positions is earlier, and therefore better, than most location strategists realise.

The Case Is Built on More Than Incentives

Every ASEAN country leads with its incentive table. The Philippines has a competitive one, BOI pioneer status grants up to six years of Income Tax Holiday under the CREATE MORE Act, with a post-ITH regime offering a reduced 20% corporate income tax rate and 100% deductions on power and training costs. PEZA-registered manufacturers add duty-free capital equipment imports, VAT zero-rating on local purchases, and streamlined customs. But incentives are a floor, not a differentiator. What actually separates the Philippines is a combination of structural advantages that no competing market can fully replicate.

English is the operating language of Philippine business

For a semiconductor fab, a hyperscale data centre, or a medtech manufacturer managing a global supply chain, this is not a soft benefit, it is a hard operational one. Compliance documentation, engineering specifications, vendor negotiations, management reporting: all of it runs in the same language as your headquarters. No other major industrial market in ASEAN offers this at scale.

The workforce is technically deep and services-capable simultaneously

The same talent pipeline that built the world’s largest BPO sector, disciplined, English-fluent, process-oriented, is now feeding into engineering, quality assurance, and advanced manufacturing roles. The Philippines produces a substantial number of engineering and technical graduates annually, with particular strength in electronics, chemical engineering, and IT-related disciplines. This is not a workforce that can only run a logistics dock. It can run a cleanroom.

The country already has an electronics manufacturing base

The Philippines is one of the world’s largest exporters of semiconductors and electronic components, this is not a new industry being invited in. Companies like Texas Instruments, Analog Devices, Intel, and Toshiba have operated semiconductor assembly and test facilities here for decades. The supplier ecosystem, the technical labour pool, and the regulatory familiarity with the sector already exist. What is new is the ambition to move further up the value chain, from assembly and test into advanced packaging, PCB, and eventually wafer-level work.

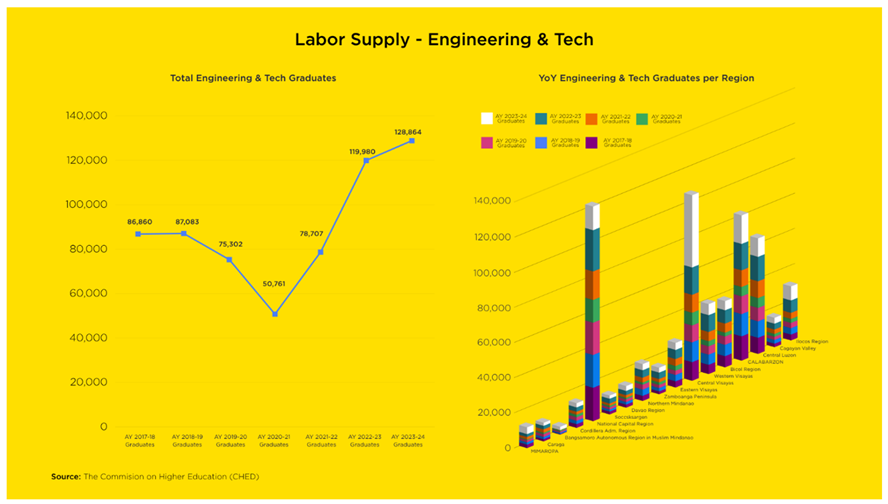

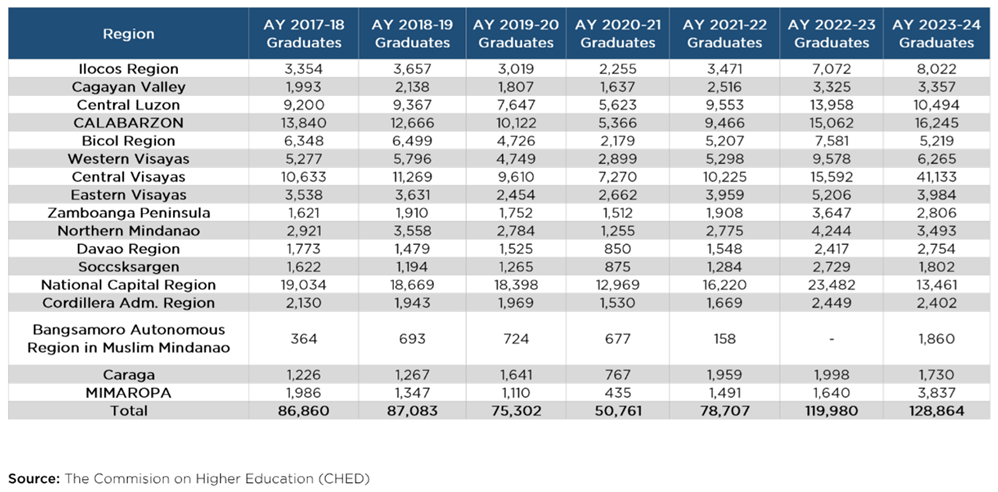

Labor Supply - Engineering & Tech

- From AY 2017–18 (86,860 graduates) to AY 2018–19 (87,033 graduates), the number of graduates remained relatively stable.

- A declining trend occurred from AY 2019–20 (75,302) to AY 2020–21 (50,781), representing the lowest number of graduates during the period. This decline may be attributed to disruptions caused by the COVID-19 pandemic.

- Beginning AY 2021–22 (78,707), the number of graduates started to recover significantly.

- A sharp increase was observed in AY 2022–23 (119,980) and continued in AY 2023–24 (128,884), reaching the highest level recorded in the dataset.

- Post-pandemic normalization and the K–12 program likely contributed to the record-high 128,884 graduates in AY 2023–24.

- Graduates surged from 86,860 (AY 2017-18) to a peak of 128,864 (AY 2023-24), a ~48% increase over 7 years

- Sharp dip in AY 2020-21 (50,761), likely due to COVID-19 disruptions

- NCR dominates every year, though it notably dropped to 13,461 in 2023-24, its lowest in the period

- CALABARZON and Central Luzon are steady runners-up, reflecting strong HEI presence outside Metro Manila

- Central Visayas exploded to 41,133 in 2023-24, skyrocketing from ~10,000 in prior years, the most dramatic regional surge

- Ilocos Region nearly doubled from 3,354 to 8,022

- BARMM (Region 15) remains the smallest contributor with inconsistent data and low numbers (~158 to 1,860)

- Soccsksargen and Zamboanga Peninsula consistently record among the lowest graduate counts

Addressing the Power Question Directly

The one metric that gives industrial occupiers pause is electricity cost. Grid retail rates in the Philippines, currently around PHP 13–14/kWh (approximately USD 0.23–0.24/kWh), are the highest in the regional comparison, roughly double Vietnam and meaningfully above Thailand.

This is real, and it deserves a direct answer rather than a footnote.

The grid rate is not the effective rate available to industrial occupiers who structure their energy procurement correctly. Three mechanisms, used in combination, can substantially close the gap:

The Green Energy Option Program (GEOP) allows any consumer with at least 50 kW of average peak demand, which any meaningful manufacturing facility would exceed, to exit the distribution utility and contract directly with a licensed renewable energy supplier. Industrial parks using GEOP have reported power cost reductions of 30 to 40 percent. Automotive and food manufacturers have seen monthly savings in the hundreds of thousands of pesos. At a 35% reduction, the effective rate drops to approximately USD 0.15/kWh, broadly comparable to Thailand.

Corporate Power Purchase Agreements (PPAs) are available to larger contestable consumers (750 kW average monthly demand and above) and allow direct contracting with solar, wind, or geothermal generators at fixed rates for up to 15 years. For a data centre or semiconductor fab with predictable, high baseload consumption, a 10–15 year PPA is both a cost optimisation tool and a balance sheet hedge against peso depreciation and fossil fuel price volatility.

On-site solar on factory rooftops and adjacent land parcels, with BOI-registered companies eligible for duty-free panel imports, can supply 30 to 50 percent of daytime consumption at amortised costs well below the grid rate. For a manufacturing facility running day shifts, the load profile aligns almost perfectly with generation.

A well-structured occupier combining GEOP or a PPA with rooftop solar can realistically achieve an effective power cost of USD 0.12–0.15/kWh. That is no longer a competitive disadvantage. It is table stakes, and it comes with a carbon intensity profile increasingly demanded by multinational supply chain audits and EU market access requirements.

The medium-term picture improves further. The Philippine Department of Energy’s Green Energy Auction roadmap targets 25 GW of new renewable capacity by 2035, backed by USD 433 billion in committed investment. More supply means structural downward pressure on rates. Occupiers locking in PPAs today are positioning themselves ahead of that curve.

What the Semiconductor Sector Specifically Needs, and Finds Here

Semiconductor investment has specific site requirements that are worth addressing directly: power reliability, water access, logistics connectivity, a skilled technical workforce, and a regulatory environment that understands the sector.

The Philippines passes on all five.

Power reliability in PEZA and LIMA-anchored industrial estates in Laguna, Batangas, and Cavite is supported by dedicated substation connections and increasingly by on-site generation, reducing exposure to grid fluctuation. Geothermal energy, in which the Philippines is the second-largest producer in Asia, provides a stable, non-weather-dependent baseload option for data centres and fabs that cannot tolerate intermittent supply.

Water access in the CALABARZON corridor, Cavite, Laguna, Batangas, Rizal, and Quezon, is industrial-grade, with established industrial estate operators managing utility provision as part of their landlord offer.

Logistics connectivity centres on the Port of Manila and the emerging Batangas port corridor, with direct RORO and container links to Singapore, Hong Kong, and major Northeast Asian ports. Air cargo through NAIA and the growing Clark and Mactan international airports supports just-in-time component supply chains.

The regulatory environment is genuinely sector-aware. The Philippines has a national semiconductor roadmap backed by government investment targets, and PEZA and BOI have dedicated fast-track channels for priority investments. The Philippines’ longstanding presence in global semiconductor supply chains means customs procedures, ITAR compliance frameworks, and export documentation processes are already understood by both government and logistics providers.

The Taiwan+1 Imperative: Why This Is Different From China+1

China+1 is a cost and tariff story. Taiwan+1 is an existential supply chain risk story, and the stakes are of a different order entirely.

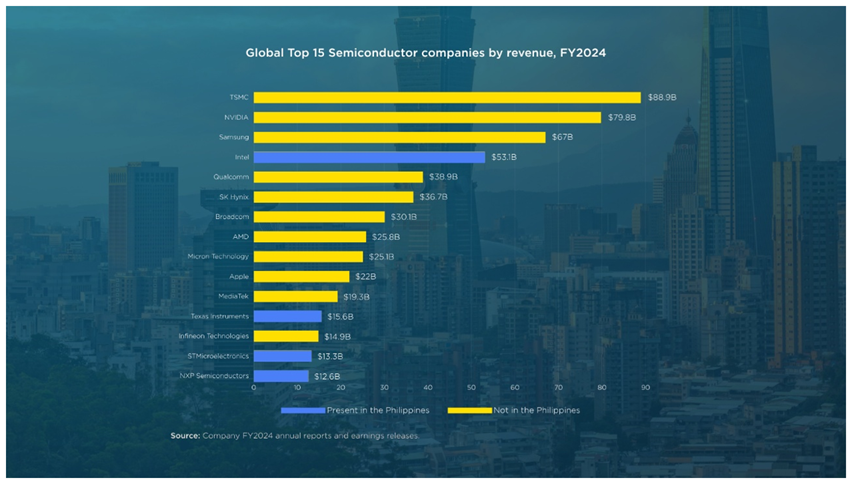

Taiwan’s semiconductor foundries hold approximately 78% of global market share and 92% of the world’s capacity for the most advanced chips. TSMC alone generated over USD 120 billion in revenue in 2025. Every major technology company, Apple, Nvidia, AMD, Qualcomm, Broadcom, manufactures its most advanced chips almost exclusively in Taiwan.

Bloomberg Economics has estimated that a Taiwan conflict would cost the global economy approximately USD 10 trillion, exceeding the economic damage from COVID-19. Building a replacement leading-edge fab takes 3–4 years and costs upward of USD 10 billion. There is no fast substitute.

The industry knows this and is responding. TSMC has committed USD 165 billion to expand into Arizona across six fabrication plants. Fabs have been established in Japan and Europe. The US CHIPS Act and equivalent policies in Japan, the EU, and India are collectively deploying hundreds of billions to redistribute at least some leading-edge capacity away from a single geographic chokepoint.

But leading-edge wafer fabrication, the headline of the Taiwan diversification story, is not where the Philippines plays, and claiming otherwise would be dishonest. Those fabs require government subsidies at sovereign scale, infrastructure investments that take a decade to mature, and talent pipelines that do not yet exist outside a handful of locations.

Where the Philippines plays well is in the broader semiconductor supply chain that surrounds the fab.

Outsourced semiconductor assembly and test (OSAT), advanced packaging, PCB manufacturing, and back-end processing represent a vast portion of total semiconductor value, and this is precisely where supply chain resilience pressure is creating the most immediate new investment. Trade frictions and geopolitical risk have already prompted active diversification of OSAT capacity into Malaysia, Vietnam, and the Philippines. The Philippines is already a credible location in the 2025–2027 OSAT expansion plans of global chipmakers, not as a future aspiration, but as an active, operating node in the global semiconductor back-end.

The Philippines is one of the world’s established OSAT hubs. Texas Instruments, Analog Devices, and others have operated assembly and test facilities here for decades. The workforce knows how to run a cleanroom. The customs and export documentation processes for semiconductor shipments are understood by both government and logistics providers. The regulatory framework PEZA, BOI, and IEAT has been handling high-value electronics exports for a generation.

The island logistics question, addressed honestly.

A fair challenge to any Philippines manufacturing thesis is the archipelago geography. Taiwan is instructive here, but the lesson is more specific than it first appears. Taiwan did not succeed despite being an island; it succeeded by concentrating on products so high in value-to-weight that logistics cost became essentially irrelevant to the economics. A wafer worth USD 50,000 fits in a carry-on bag. A container of packaged semiconductors is worth more than a container of almost anything else manufactured in Asia.

The Philippines has the same value-density argument available to it for electronics and semiconductor back-end work, and this is exactly the segment the Taiwan+1 thesis targets. Logistics cost as a percentage of product value for a shipment of packaged ICs or advanced PCBs out of a CALABARZON PEZA zone is negligible. The Batangas port corridor, increasingly the preferred logistics gateway for Southern Luzon industrial output, handles this traffic today.

The honest caveat is that the Philippines’ archipelago geography creates domestic logistics complexity that Taiwan never had. Components moving between islands for intermediate processing add cost

and time that a single-island competitor does not face. This matters more for lower-value, higher-volume manufacturing, garments, furniture, consumer goods, where freight cost as a percentage of product value is significant. For electronics and semiconductors, it is a manageable friction, not a disqualifying one. Smart supply chain design concentrates the relevant production steps within a single industrial corridor, CALABARZON for Southern Luzon, or Clark for Central Luzon, rather than distributing them across the archipelago.

The Taiwan+1 opportunity for the Philippines is real, it is active, and it is in the right segment. The question for semiconductor companies is not whether to diversify away from Taiwan-concentrated supply chains, that decision has already been made at most major chipmakers’ board level. The question is which resilience destinations are being built out, and whether the Philippines is on the shortlist. For back-end semiconductor, OSAT, and advanced packaging, it should be.

Data Centres: The Infrastructure Moment

Southeast Asia’s data centre market is in a structural build-out cycle driven by hyperscale cloud, AI infrastructure, and regional data sovereignty requirements. Singapore remains the reference market, but its moratorium-constrained land supply and rising power costs have pushed operators to look at alternatives. Malaysia (Johor) and Thailand have absorbed significant demand. The Philippines is the next logical node.

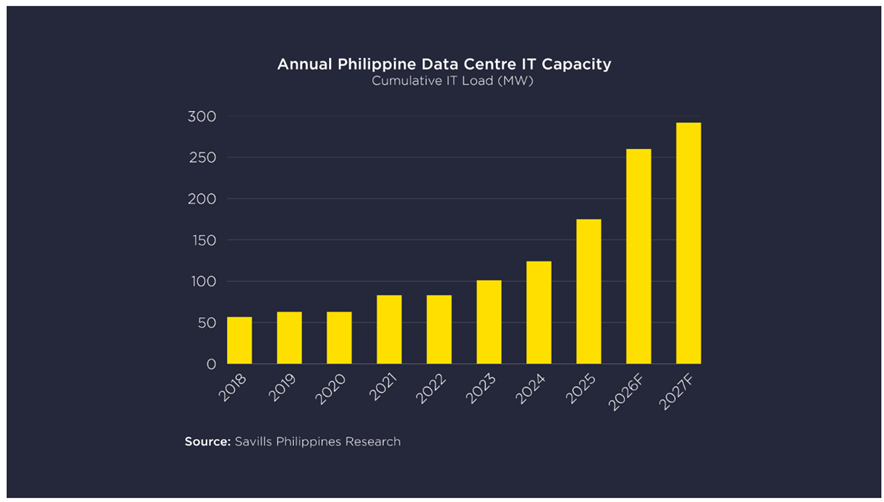

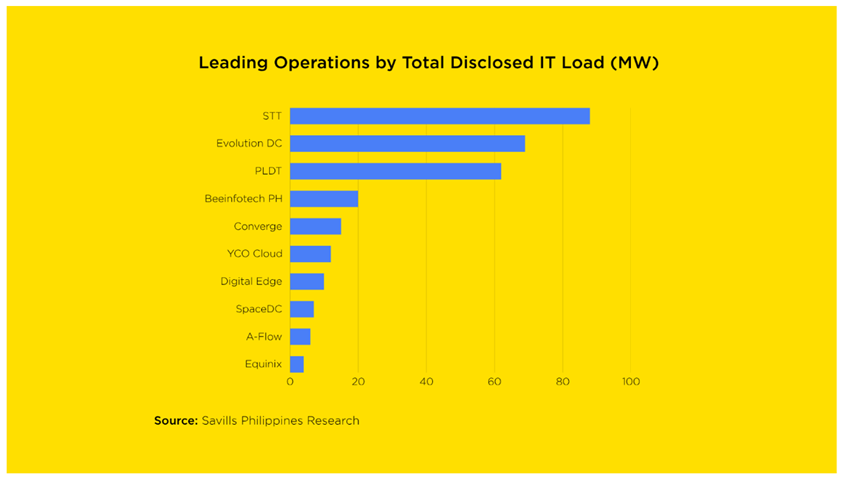

The build-out is already visible in the domestic supply pipeline. Cumulative operational IT capacity among facilities with disclosed power specifications has nearly tripled since 2019, with the steepest additions arriving in 2024–2025 as hyperscale-grade campuses such as STT Fairview and ePLDT VITRO Sta. Rosa came online.

The case is straightforward: a population of over 115 million people with one of the highest social media and mobile internet penetration rates in the world, a BPO sector generating constant data processing demand, and a government actively courting hyperscale investment with BOI incentives and streamlined approvals through the Green Lane programme.

The power question for data centres is addressed by the same mechanisms above, with the additional advantage that geothermal baseload, available through direct PPAs with First Gen and other licensed suppliers, offers the kind of 24/7 reliable clean power that hyperscale operators require for both operational and ESG purposes.

Land is available. Large contiguous plots in Clark, Batangas, Laguna, and Metro Manila’s fringe markets can accommodate the footprint requirements of hyperscale campuses. Connectivity infrastructure, subsea cable landing stations, IX points, fibre backbone, is already present and expanding. The market is also concentrating around a small group of scaled operators. By total disclosed IT load, ePLDT VITRO and ST Telemedia (STT) together account for the majority of capacity among facilities with published specifications, a structure that mirrors the carrier-neutral colocation consolidation seen across the wider region.

A Note for Industrial Estate Developers: Energy Is Now Part of Your Product

The occupier case above has a direct implication for developers: the industrial estates that will attract the next wave of semiconductor, data centre, and advanced manufacturing investment are not simply those with the cheapest land or the best PEZA registration. They are the ones that have solved the power problem before the occupier even asks the question.

This is a genuine shift in what it means to be a competitive industrial landlord in the Philippines.

The opportunity is real

Grid retail rates have risen 17–18% year-on-year as of mid-2026. Every time the grid goes up, a developer who has locked in captive solar or a long-term bulk PPA for their estate widens the gap between what their locators pay and what they would pay anywhere else. That gap is a marketable, quantifiable asset, not a sustainability footnote. Industrial parks that have adopted estate-wide renewable procurement have reported power cost reductions of 30 to 40 percent for their locators. For a semiconductor fab or data centre operator running continuous, high-draw operations, that saving directly affects their decision of which site to sign.

Rental premium follows. Developers who can offer guaranteed below-grid power as part of the tenancy package can justify higher rents, and still leave the occupier ahead on total operating cost. The best industrial estates in the CALABARZON corridor already command PHP 280–290/sqm in average rents. Estates with a credible energy value proposition have room to push beyond that ceiling as demand from power-sensitive occupiers intensifies.

How to think about it in tiers

Not every developer needs to become a power company. The smarter framing is a staged approach:

At the minimum, master-plan the estate for energy from day one, roof orientations, structural loadings, and common area layouts designed to accommodate solar across the entire park. Pre-negotiate a GEOP or bulk PPA so locators can access competitive RE rates immediately, without each occupier having to run their own procurement process. This costs relatively little and is a strong marketing differentiator.

The next tier is captive solar and battery storage for common infrastructure, the developer’s own consumption across shared utilities, security, and wastewater. This is wholly within the developer’s operating perimeter, avoids regulatory complexity around power resale, and signals to prospective locators that the estate takes energy seriously.

For developers with the capital appetite and the right legal structure, the full model, offering guaranteed below-grid power as a bundled feature of tenancy, potentially through a separate energy subsidiary or a JV with a licensed renewable energy developer, is the premium positioning play. This is already happening at scale elsewhere in the region: industrial estate developers partnering with independent power producers to anchor captive generation inside the estate boundary, creating a vertically integrated product that neither a locator nor a competing landlord can easily replicate.

The regulatory reality

Selling electricity to third parties, including your own locators, requires licensing under EPIRA and DOE rules. A developer pursuing the full captive model needs this structured correctly from the start, ideally through a separate entity or an accredited RE supplier partnership. This is not a dealbreaker; it is a planning requirement. The developers who treat it as an afterthought will face delays. Those who build it into the project structure early will have a product their competitors cannot match.

The bottom line for developers

The Philippines is assembling the conditions for a significant step-up in industrial investment. The occupiers coming, in semiconductors, data centres, advanced electronics, are not choosing sites on land cost alone. They are choosing on total operating cost, energy certainty, ESG credentials, and supply chain resilience. A developer who has embedded a credible energy strategy into their estate is not just selling land. They are selling certainty. In a market where power cost has historically been the first objection, that is a powerful position to be in.

The Honest Competitive Position

The Philippines is not the cheapest location in ASEAN. Vietnam and Indonesia offer lower labour costs forvolume manufacturing. Thailand offers a deeper automotive supplier base and a longer CIT holiday for greenfield projects.

What the Philippines offers is different: an English-fluent, technically capable workforce; an existing semiconductor and electronics export base that de-risks sector entry; a renewable energy procurement environment that can neutralise the power cost gap for structured buyers; and a domestic market of 115 million people that provides a distribution anchor no other comparable ASEAN market can match at the same income level.

For occupiers whose location decision is driven by talent quality, language capability, supply chain maturity in electronics, and long-term market access, rather than purely by land cost per square metre, the Philippines belongs in the shortlist, not the footnote.

How Savills Philippines Can Help

Savills Philippines advises industrial occupiers, data centre operators, manufacturing investors, and estate developers across the full site selection and development cycle, from location strategy and PEZA/BOI zone comparison to site search, commercial negotiation, and coordination with legal, construction, and energy procurement partners.

For occupiers and manufacturers, we provide:

- Consultancy, Land & Technical Valuation Study on target location/ property

- Industrial land, factory, and warehouse site search and shortlisting

- Market briefing and zone-by-zone location analysis (CALABARZON, Clark, Cebu, Davao)

- Coordination with legal, project management, and financing partners

- Negotiate Built-to-suit and/or ready-built factory options

- Project Management, Construction Management

- Network & IT Equipment Procurement and Installment coordination

- Building Shell & Power Base building readiness and connectivity coordination

- Fit-Out Building Security and fire suppression system delivery

- Fit-Out Mechanical Cooling system design and installation coordination

- Fit-Out Electrical Power backup and distribution coordination

- Critical Facilities Management Ongoing DC facilities operations and maintenance oversight

For industrial estate developers, we provide:

- Land acquisition, feasibility, and estate planning advisory

- Occupier demand analysis and target sector positioning

- Energy infrastructure strategy and RE partnership introductions

- Leasing strategy, rent benchmarking, and Broker Opinion of Value

- Sale-and-leaseback and investment structuring

- Project Management, Construction Management

Written by

- Philippines industrial sector

- Philippines industrial real estate

- industrial real estate Philippines

- commercial and residential properties

- warehouse development Philippines